It's Never Too Early -- Or Too Late -- To Start Investing for Retirement

"Time is money." -- Benjamin Franklin

Benjamin Franklin may not have been referring to the effect of time on money accumulating in an employer-sponsored retirement plan, but his words certainly ring true to today's investor. That's because time is one of the best allies an investor has. But even if you didn't start investing in your plan until later in life, there's another old saying that you may want to heed -- "Better late than never."

Triple Feature

No matter where you are in your life or how much you have in your retirement account, your employer-sponsored retirement plan may have features that could help you build your nest egg.

First, it offers the advantage of compounding -- that is, earnings on an investment's earnings -- tax free until withdrawal. Second, many plans offer matching contributions that are made on your behalf by your employer. Third, your plan likely offers you a range of funds from which to choose. The earlier you put these elements to work in your plan, the better off you'll likely be in the long run.

Investing Can Begin at 40

Now we all know life happens and not all of us start building nest eggs at such a young age. But what about when you turn 40 and suddenly realize you have saved little or nothing for retirement? Don't panic. You can still make up for lost time, but you may need to put your plan into high gear.

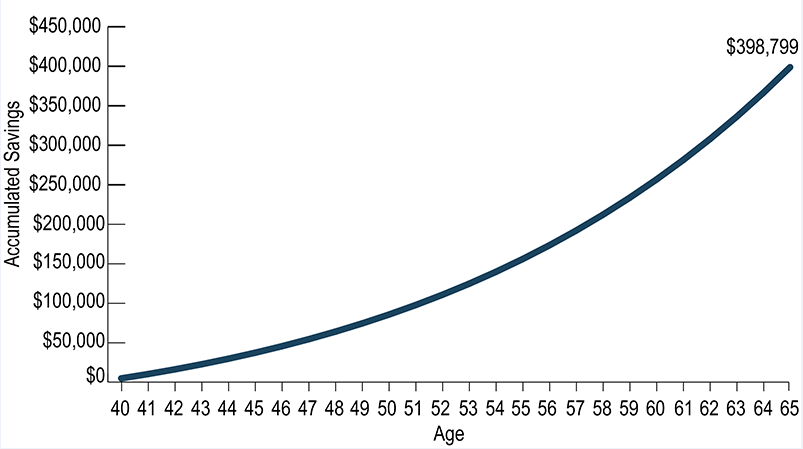

First, start contributing as much as possible to your plan. Starting at 5% and increasing it 2% each year until you reach the company maximum might be a place to begin. Then it may help to invest in more aggressive funds, such as stock funds, which are subject to short-term volatility but have historically generated higher long-term returns than all other asset classes. The accompanying chart shows you how much you might potentially accumulate in 25 years. Note that this example is hypothetical. Your results will vary.

| How Your Savings Could Grow |

|

As you can see, for someone who starts saving at age 40 and saves steadily until age 65, it may be possible to accumulate a significant nest egg.1

Whether you're fresh out of college, approaching retirement, or somewhere in between, there's no time like the present to take advantage of your employer-sponsored retirement plan.

1This hypothetical example is for illustrative purposes only. Your results will differ. It assumes that the saver earns $50,000 per year at the start of the program and saves 10% of income per year while earning 6% total return per year. It also assumes that the saver's income grows 3% per year and that growth would be reflected in the annual contributions.

© 2020 SS&C Technologies, Inc.